In probability theory, Bienaymé's identity is a formula for the variance of random variables which are themselves sums of random variables. I provide a little intuition for the identity and then prove it.

Published

04 January 2024

Let Bn denote a random variable which is itself the sum of n random

variables,

Bn:=i=1∑nXi.(1)

Bienaymé’s identity, named after the French statistician Irénée-Jules

Bienaymé,

states that the variance of Bn is

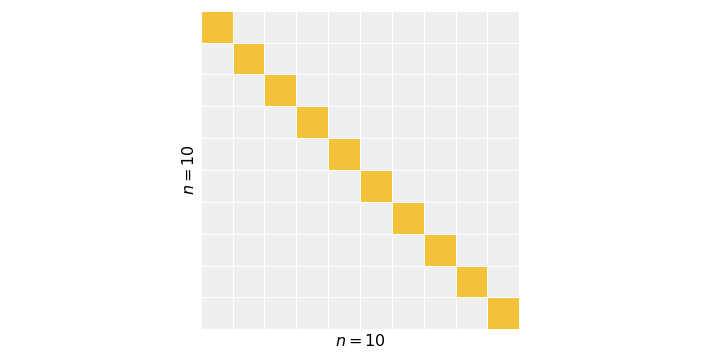

In either case, we can visualize this identity as summing the elements of the

covariance matrix of the vector [X1,…,Xn] (Figure 1). In Equation 2, we break the sum into the

diagonal and off-diagonal elements, while in Equation 4, we denote the

diagonal elements with the same notation as the off-diagonal elements.

Figure 1. Visualization of Bienaymé's

identity. The matrix represents an n×n covariance matrix of the

vector [X1,…,Xn]. The variances or diagonal elements (gold) are captured in the

middle sum in Equation 2, while the covariances or off-diagonal elements (gray) are

captured in the right sum in Equation 2.

If we write the covariance in terms of Pearson’s correlation coefficient ρ,

then the identity in Equation 3 becomes

V[Bn]=i,j=1∑nρijV[Xi]V[Xj].(5)

An important special case of Bienaymé’s identity is when the random variables

are independent or uncorrelated (ρ=0). In either case, the covariance between the

random variables is zero or

With a little thought, Bienaymé’s identity is fairly intuitive. If we add random

variables together, then we are compounding uncertainty. However, that

uncertainty is less if the elements are independent or uncorrelated, in which

case their uncertainty is unrelated. But in the worst case, all random variables

are highly correlated with ρ=1, which maximizes the variance of Bn. Alternatively, in the best case, all random variables are highly

anti-correlated with ρ=−1, which minimizes the variance of Bn.

Finally, proving Bienaymé’s identity really amounts to understanding how to

square a sum of terms. In general, it is true that